A lot can change in just one year. Last summer, benefits professionals anticipated the likely election of Hillary Clinton and the continuation and possible expansion of the Affordable Care Act. Now they are adjusting to the brave new world of a Donald Trump administration and an uncertain future for national health policy.

Related: Trump approval rating tumbles after health care vote

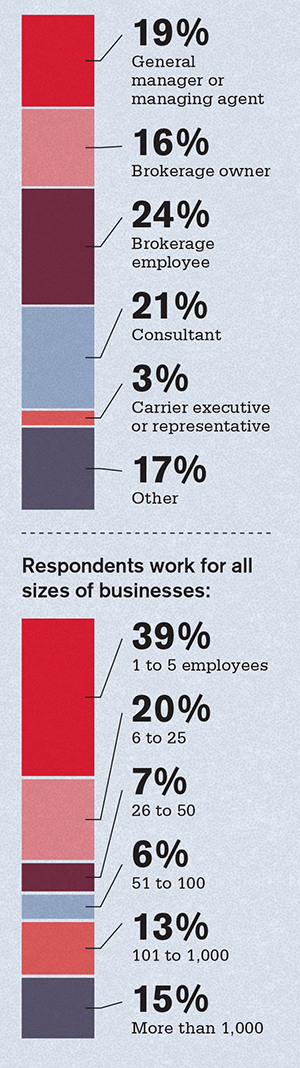

But the industry is taking the changes in stride, according to the just-released 2017 BenefitsPRO Health Care Survey. Nearly 350 professionals from all industry sectors (see sidebar) shared their thoughts on current issues and what lies ahead for the remainder of 2017 and beyond.

More than one-half of respondents (55 percent) believe the Trump presidency will have a positive effect on their business, while 32 percent expect it to have a negative impact. Exactly one-half would like to see the ACA retained and repaired, while 28 percent prefer a gradual repeal and replace, and 22 percent want it repealed and replaced immediately.

Financial pulse

Although political issues may be fun to debate, sales will always be the lifeblood of the industry. Some of the most revealing responses in the survey show how benefits providers of all sizes view their financial situations. This starts with retention, because keeping a current client is every bit as important as gaining a new one.

Related: Small biz owners sound off on health care & Trump

The most significant client losses were in small-group accounts (less than 100 lives), where 47 percent of respondents report between 1 percent and 24 percent of their clients dropped coverage in 2016. As might be expected, the ability to maintain coverage increased as the size of the business increased.

Twenty-five percent of brokers report their mid-market clients (101 to 500 lives) dropped coverage last year. This percentage drops to 14 percent for large groups (501 to 3,000 lives) and 7 percent for national accounts (more than 3,000 lives). Sixty-four percent of those surveyed expect the percentage of groups dropping coverage to stay the same in 2017, while equal percentages (14 percent) believe it will increase or decrease a little.

Despite the losses, most brokers are optimistic about their prospects for the rest of 2017. More than half (54 percent) of those who responded expect average health insurance commissions to increase or at least remain the same this year. Thirty percent anticipate a decrease, but by no more than 25 percent. Only 4 percent expect commissions to drop by more than half. Seventy-eight percent expect total compensation from ancillary or bundled product sales to increase this year, while not a single respondent expects decreased sales.

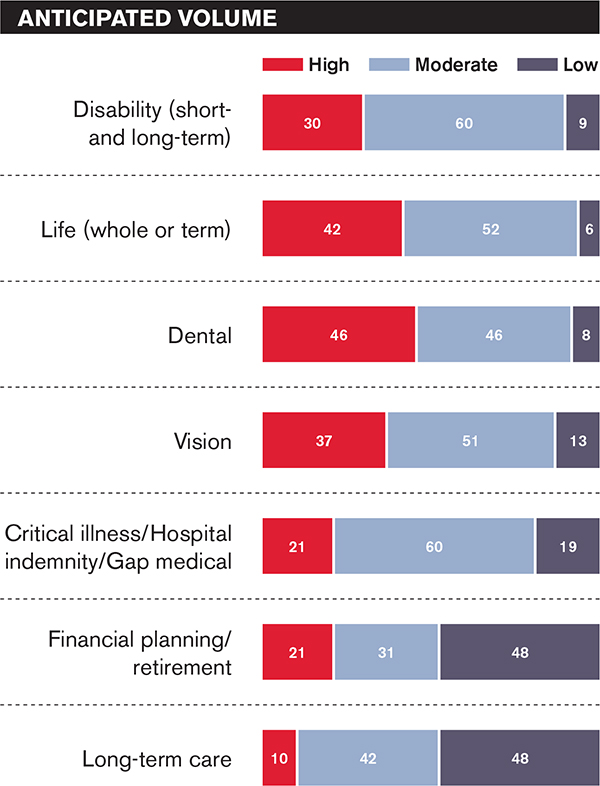

Brokers are even more optimistic about health insurance prospects for 2018. Fifty-six percent look forward to steady or increased commissions, while only 18 percent expect a decrease. A growing portfolio of ancillary products to sell may be one reason for this optimism. BenefitsPRO asked which products they intend to sell and what volume of each they anticipate.

Given these expectations, it's no surprise the voluntary benefit sector continues to grow. Fifty-five percent of respondents are neutral or strongly agree with the statement that they will use voluntary benefits to offset anticipated commission losses from health insurance this year. The same percentage views private exchanges as an opportunity to sell more voluntary products.

Brokers have a good idea of what it will take for them to sell more voluntary products. When asked to rank their No. 1 criterion, they say lower prices (42 percent); simpler and more convenient enrollment options (28 percent); increased member and employer education (17 percent); consumer life-stage bundles (8 percent); and carriers with better brands (8 percent).

Related: 6 non-traditional voluntary trends for 2017

State exchange insights

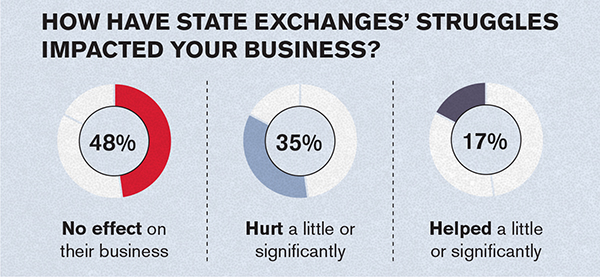

Although problems facing state exchanges under the ACA have been well publicized, their impact on brokers appears to be mixed. Nearly one-half (48 percent) of survey respondents say the struggles of these exchanges have had no effect on their business. Thirty-five percent have been hurt a little or significantly, while 17 percent have been helped a little or significantly.

One clue as to why the exchanges have no effect on so many brokers is there is little demand to help individuals enroll. Thirty-four percent of respondents say their book of business doesn't handle individuals, and another 37 percent say demand is either weak or non-existent. No wonder less than 10 percent say enrolling individuals on the public exchange is worth the effort.

What about private exchanges? Nearly 6 in 10 of those responding say they do not have a private exchange partner for enrollment and benefits administration. Twenty-six percent work with a single private exchange partner, and 16 percent use two. Only 16 percent have invested in developing their own proprietary private exchange technology.

Related: Brokers giving up on ACA

The nature of group clients continues to change. Nearly one-half (49 percent) of brokers say more of their accounts will use defined contribution funding this year. The percentage varies by the size of the group. Brokers expect a move to defined contribution by between 1 percent and 24 percent of small groups; 39 percent of small-market groups; 21 percent of large groups; and 15 percent of national accounts.

Enrollment 101

The bottom line in the brokerage business is to engage with individual or group clients and get them to enroll. Face-to-face meetings are overwhelmingly the most common way to make this happen.

Related: Open enrollment: When preparation meets opportunity

Fifty-three percent of respondents say meeting in a group setting at the worksite is the primary enrollment technique, while 36 percent cited one-on-one meetings in the workplace. However, 39 percent say their top method is using an electronic enrollment tool independently.

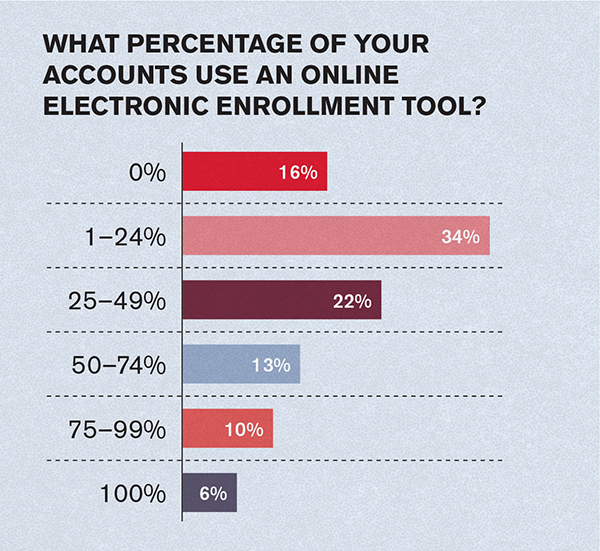

BenefitsPRO asked brokers what percentage of their clients currently use an online electronic enrollment tool. Only 16 percent say none do, and 6 percent say they all use this technology. Thirty-four percent say between 1 percent and 24 percent do; 22 percent say from 25 percent to 49 percent; 13 percent responded 50 percent to 74 percent; and 10 percent say 75 percent to 100 percent.

Sixty-five percent of brokers say offering enrollment or benefit administration technology and/or an online solution to clients is a critical component of their value proposition. Only 10 percent disagree.

Carrier criteria

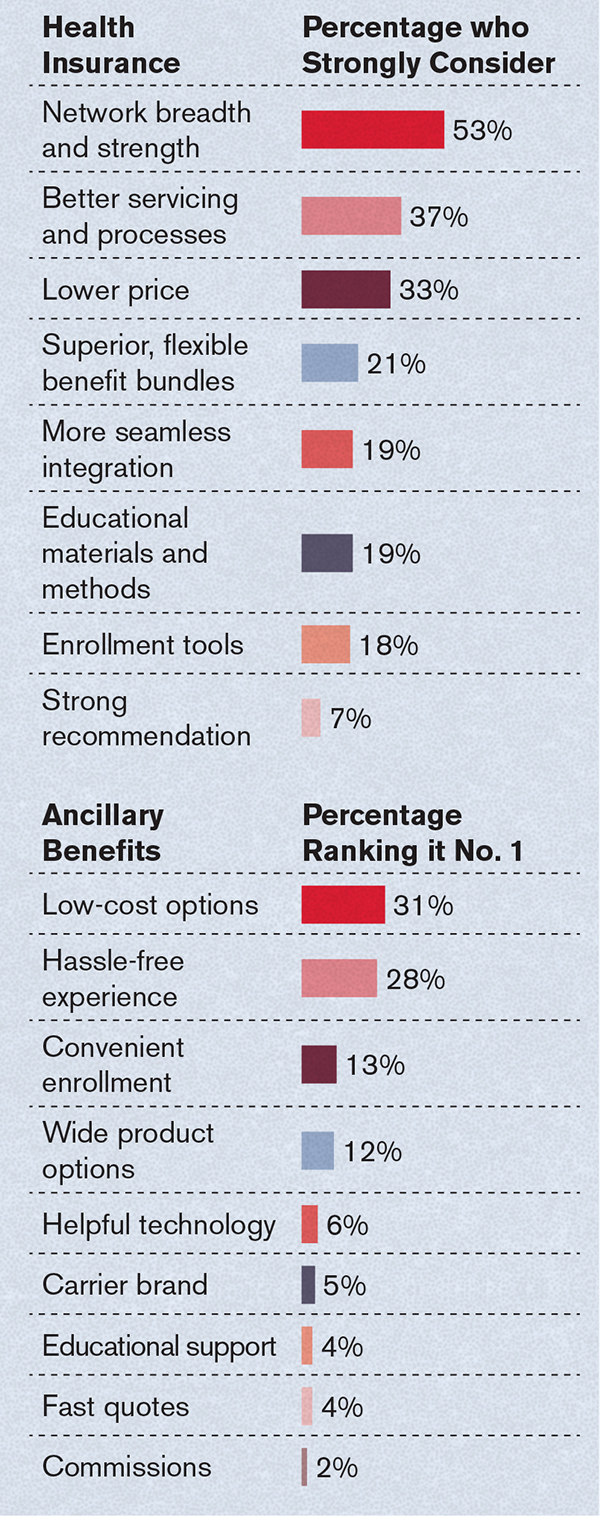

Clearly, the benefits selling industry is changing, and carriers need to adjust or be left behind. Brokers have clear ideas of what they expect from carriers, both for health insurance and ancillary products. The survey asked which factors they strongly consider in both categories.

A look ahead

BenefitsPRO asked those taking the survey to look into their crystal ball and predict what may happen both industrywide and in their own companies in the future. It looks like the merger-and-acquisition trend will continue over the next five years:

-

Twenty-seven percent expect their organization to acquire or merge with another broker/agent organization.

-

The same percentage believes their company will buy out the book of business of a retiring broker or agent.

-

Fourteen percent look for another broker/agent to acquire their organization.

-

Fourteen percent also say their company will leave the health insurance brokerage business.

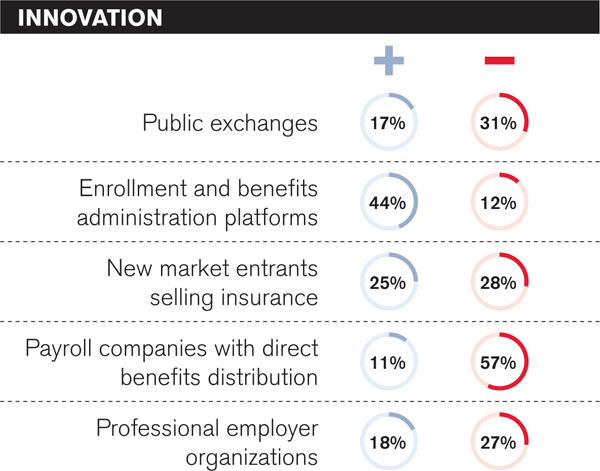

Brokers anticipate several innovations that could affect business performance during the next three years. However, they don't always agree on whether the impact will be positive or negative.

Many brokers report they expect to increase their focus on the following services, which they already offer:

-

Promoting ancillary insurance coverage, 84 percent

-

Promoting health plan consumer engagement and health and wellness programs, 58 percent.

-

Promoting third-party consumer engagement and health and wellness programs, 43 percent.

And as for potential threats, 53 percent find the new wave of disruptive companies entering the industry to be “somewhat concerning.”

Will any or all of these predictions come to pass? As the election of 2016 showed, trying to predict the future can be a challenge. Be sure to check out the 2018 survey to stay on top of the latest trends.

Meet the survey respondents

The BenefitsPRO 2017 Health Care Survey was conducted from February through May. The 336 respondents represented most key positions:

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

Alan Goforth

Alan Goforth is a freelance writer in suburban Kansas City. In addition to freelancing for several publications, he has written a dozen books about sports and other topics.