Although most people plan to work until 65 or later, about half of people who retire sooner than they had planned do so because of events beyond their control. (Photo: Shutterstock)

Although most people plan to work until 65 or later, about half of people who retire sooner than they had planned do so because of events beyond their control. (Photo: Shutterstock)

Most financial experts agree that a retirement crisis is either looming on the horizon or already here, due to Americans' insufficient savings.

The Schwartz Center for Economic Policy Analysis at the New School estimates that roughly 40% of Americans, or 2 out of every 5 who are currently considered 'middle-class' based on their income, will fall into poverty or near poverty by the time they reach 65.

The authors of the study defined middle class as an individual or couple earning more than twice the federal poverty level before age 65 (currently $12,140 for an individual, $16,460 for a couple) and then earning less than that threshold after age 65.

Lead researcher Teresa Ghilarducci, using data from the US Census Bureau, predicts that 8.5 million middle-class older workers and their spouses will be downwardly mobile in retirement, falling into poverty or near poverty after reaching 65.

And the risk increases as people get older. Those over 80 are 30% more likely to be poor than those aged 65-69.

She cites three main reasons that the risk of poverty increases as retirees get older: depressed earnings, decreased asset values, and increases in health care costs, which are all likely to accelerate future old-age poverty rates.

Related to these factors is an additional issue. The most common age for retirement is 62, the earliest possible age to begin receiving Social Security. Although most people plan to work until 65 or later, about half of people who retire sooner than they had planned do so because of events beyond their control — their own health issues or needing to provide caretaking for a loved one, or getting laid off from a job and being unable to find another one.

The problem is that while it's possible to begin receiving Social Security payments as early as age 62, the benefit amount is then permanently reduced to 75% of what it would normally be at an individual's full retirement age.

In 2017, the average monthly benefit for those age 62 was only $1,112. That's not much above the federal poverty level of $1,011.66 a month or $12,140 annually for an individual.

Yet 25% of people in a recent survey expect that Social Security will be their primary source of income in retirement. An additional issue is that claiming Social Security benefits early will also permanently reduce the benefit for a surviving spouse when the primary earner passes away.

Living on Social Security alone

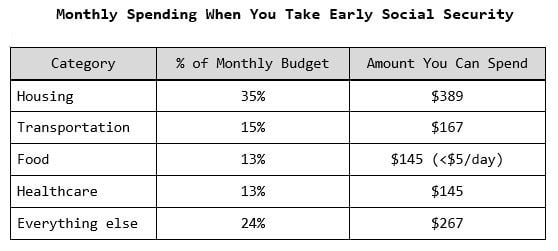

What does life on a monthly budget of $1,112 look like? Based on data from the Bureau of Labor Statistics, the average household over 65 spends $45,756 per year, or roughly $3,800 a month. Broken out by category, retirees spend about 35% of their budget on housing, 15% on transportation, 13% on health care, and 13% on food, leaving about 24% for all other discretionary spending.

Using those same percentages applied to the average Social Security check for someone age 62, here's how much money an individual would have:

Table: Martha Brown Menard, PhD

Table: Martha Brown Menard, PhDEven for those retirees who have paid off their mortgage and own their home outright, a housing budget of less than $400 a month and a grocery budget of less than $5 a day is hardly realistic.

And $145 a month barely covers Medicare Part B, let alone any prescription medications. There's not much left over at the end of the month for utilities, clothing, replacing household items, or even a Netflix subscription, assuming you have a capable streaming device to watch it on. Doubling these amounts for a couple still means making do on an annual income of $24,280.

No easy solutions

Compounding the problem is the lack of access to retirement savings plans for 35% of private sector workers, and the low levels of retirement savings for those over 50. Annual studies have shown that 42% of Americans have saved less than $10,000 for retirement — not enough for even 6 months worth of living expenses.

Other surveys have shown that the main reason that people aren't saving for retirement is that they are struggling to pay their bills.

It's a grim picture, and there aren't any easy or simple solutions. Clearly, people need to spend less and save more now, so that their money has more time to grow. Working longer can help too.

The bottom line is that most people need help to reach a state of financial well-being so that they can afford to save for retirement and are looking to plan sponsors to provide that support— financial wellness is quickly becoming one of the most popular employee benefits.

And financial wellness technology can make personalized financial advice both possible and scalable for retirement plan advisors.

Dr. Martha Brown Menard is the Senior Researcher and data diva for Questis. She is a research scientist, financial wellness coach, and member of the Association for Financial Counseling and Planning Education. She is passionate about democratizing personalized financial guidance through scalable and configurable technology.

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.