Today, over 60 percent of all employers in the U.S. self-insure their employee medical benefits. And the self-insurance rate is poised to grow even more. This may come as a surprise to those used to the days, not long ago, when the majority of employers purchased a fully insured product from an insurance company, a Blue Cross Blue Shield organization, or a Health Maintenance Organization (HMO).

Today, over 60 percent of all employers in the U.S. self-insure their employee medical benefits. And the self-insurance rate is poised to grow even more. This may come as a surprise to those used to the days, not long ago, when the majority of employers purchased a fully insured product from an insurance company, a Blue Cross Blue Shield organization, or a Health Maintenance Organization (HMO).

A growing market

Health plans and providers increasingly view self-funding as a viable market opportunity. Many health providers that initially chose to self-fund their own benefit plan, for example, now desire to introduce a self-funded product in their market. It makes good business sense. Self-funding offers an opportunity to drive more patients to provider-owned facilities and capitalize on synergies with employer clients and distribution partners.

With the increased popularity of self-funding, many health plans have become active in the employer stop loss (ESL) business – and many more are seeking to enter. ESL insurance allows employers to self-fund while protecting against catastrophic or unpredictable losses, as the insurer provides coverage for losses that exceed defined limits. Exposure from specialty drugs and continued growth in $1 million+ claims are among the high-cost growth drivers for ESL insurance.

Many regionally based health carriers and several large nationally recognized group life and disability carriers have entered or are looking to enter the ESL market. Since the passage of the Affordable Care Act (ACA) in 2010, the growth in the ESL market has accelerated from a compound annual growth rate (CAGR) of 7 percent from 2006-2011 to a 12% CAGR from 2011-2015, with annual ESL premiums now totaling $17 billion. At this point, there is no indication that legislation to replace/repeal the ACA will have a significant impact on this sustained growth.

The opportunity is clear. The challenge: how to gain access to the ESL market and build business once there.

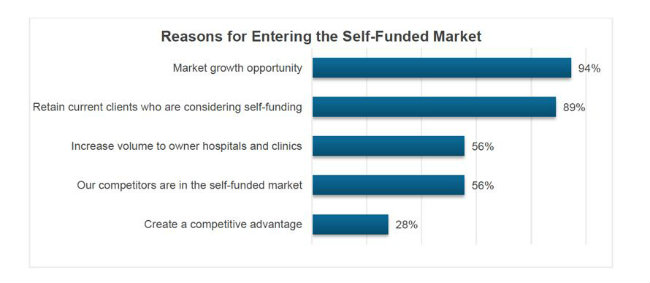

What brokers are seeing

In May 2018, RGA conducted a survey of brokers about the ESL market, the participants, and the opportunity. The results reaffirmed the need for solutions to facilitate health plans' entrance into and success within the ESL space.

The top two reasons for health plans entering the self-funded market, as cited by brokers, point to a recognition of the significant opportunity presented by this market from both new and existing customers:

So how do you capitalize on this opportunity? We also asked brokers, who observed their clients' experiences, what they considered the top three factors for success in the self-funded market. Competitive ESL rates topped the list, cited by 85 percent of respondents. The strength of the regional network came next, followed closely by competitive administrative services only (ASO) arrangements and network access fees. Other factors indicated by brokers, outside of our list of choices, included strong broker relationships and competitive broker commissions.

Interestingly, while competitive ESL rates ranks number one as a critical factor for success, this is not considered the top market challenge. That spot belongs to sales training, which was listed as a top-three market challenge by 70 percent of respondents. Having an understanding of the self-funded market may be even more important, as 50% of respondents ranked it highest. Potential sales channel conflict and uncertainty as to whether it would be best to build, buy or outsource required capabilities were other possible market challenges raised by participants.

Given these challenges, does outsourcing offer a path to market entry? In line with a concern about competitive rates and fees, brokers feel that their clients are most likely to outsource the pricing function, policy forms and rate filings, and case level underwriting. Sales training was also cited by 50% of respondents as something that health plans are likely to seek from a third party – likely reflective of the previously indicated market challenges of acquiring both sales training and a good understanding of self-funding.

The market has spoken: the era of self-funding is here. While health plans and others seek strategies to enter into or advance within the ESL space, those industry players developing solutions to facilitate this process will position themselves for significant growth.

David Sipprell is Senior Vice President, Managed Care Stop Loss Turnkey, at RGA.

Eva Goldstein is Assistant Vice President, Strategic Partnerships, at RGA.

Leigh Allen is Director, Global Surveys and Distribution Research, at RGA.

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

")