7 questions about health insurance for 2020

Here are some of the things we'll ask about, other than the two obvious things.

{kind=link}

The U.S. health insurance markets look as if they could be stable in 2020, or could turn eight-dimensional somersaults.

The federal courts continue to wrestle with Texas v. Azar, a court case that could lead to a little, some, all or none of the Affordable Care Act to be tossed out immediately, after a transitional period, or never.

Related: The political landscape in 2020: Chaos is the new normal

The general elections on Nov. 3, 2020, could give the United States a federal government with anything from a socialist philosophy, to a passion for a health finance system based mainly on health savings accounts, to a system directed by Vladimir Putin’s dogs.

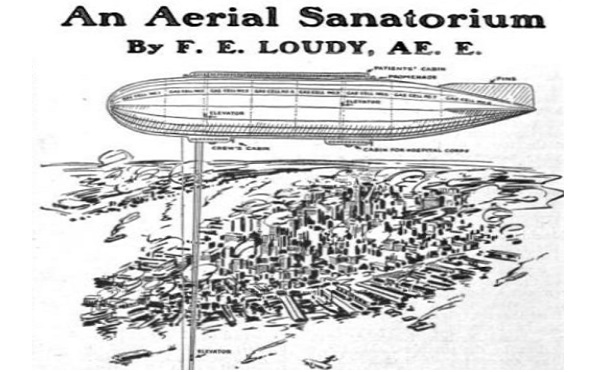

One way to see how difficult making forecasts about health care and health insurance can be is to look at how publications were covering the topics 100 years ago. In the October 1920 issue of Science and Invention magazine, for example, a writer suggested that New York could help the city’s many tuberculosis patients by putting them in a sanatorium in a giant blimp.

The writer missed the fact that airplanes would mostly replace blimps, and that scientists would come up with chemicals (antibiotics) capable of curing tuberculosis. But the writer was thinking about an important question: What should the country do about people with TB?

Here are seven questions that could shape our health insurance reporting between now and the day the courts rule on Texas v. Azar, or Nov. 3, whichever comes first.

1. Will the ACA public health insurance exchange programs outlast the ACA?

EHealth Inc., a commercial web-based supermarket for health insurance, has relationships with about 990,000 people, and a market capitalization level, or total value, of about $2 billion, or about $2,000 member.

Covered California, the state-based ACA exchange in California, has about 1.4 million members, and HealthCare.gov, the U.S. Department of Health and Human Services ACA exchange program, has about 8.3 million members.

If the per-member value of those programs is comparable to the per-member value of eHealth, Covered California might be worth $2.8 billion, and HealthCare.gov might be worth $17 billion.

Would the disappearance of the ACA really make the value of those ACA exchange programs just go poof, or will the potential market value of the programs keep the programs alive, in one form or another, even if the health law blows away?

2. Will short-term health insurance policies turn into the next generation of individual major medical insurance policies?

Issuers of short-term health insurance policies seem to be assuming that, if they want the policies to be regarded as individual major medical alternatives, the policies have to provide the kind of coverage the consumers expect from major medical coverage, with only a moderate level of medical underwriting.

The result: the newest short-term health insurance policies sound as if they resemble what might have passed for being pretty good individual major medical insurance policies in 2013, before most of the ACA individual major medical benefits, underwriting and pricing rules took effect.

The new short-term policies seem to come with annual benefits caps in the $1 million to $2 million range, lower deductibles than fully ACA-compliant policies, broader provider networks than ACA-compliant policies, and leaner behavioral health benefits than what ACA-compliant policies claim to provide.

One question might be whether the ACA drafters designed an individual major medical product that did more to make hospitals and transplant surgeons happy than to please consumers, and whether the new, beefed super short-term health insurance policies simply come a lot closer to providing the right balance between coverage richness and affordability?

3. Will Haven Healthcare matter?

Amazon, JPMorgan and Berkshire Hathaway started this nonprofit, Boston-based health coverage provider to revolutionize health insurance.

In 2020, Haven Healthcare will help Amazon and JPMorgan offer plans with wellness incentives, without deductibles, with clear patient out-of-pocket cost-sharing expectations, and with services provided by Aetna and Cigna.

This may be the year when the program starts to show whether it will really lead to big changes in health coverage or just another

4. Will states figure out a way to police health care cost sharing ministries?

Health care cost sharing ministries are to health insurance what church-based daycare centers are to commercial daycare centers. The ACA exempts them from ACA rules. Many states have been leery of the idea of trying to impose state oversight on religious organizations that happen to pay for members health care.

But many state insurance regulators have expressed concerns about the ministries, and even some of the ministries themselves appear to be open to some regulation, to keep bad apples from ruining the barrel.

5. Will life insurance companies become the health cops?

The ACA and health insurance-related privacy and discrimination rules have limited health insurers’ ability to offer wellness incentives.

Life insurers have more flexibility. John Hancock and other life insurers have developed aggressive, app-linked wellness incentives. That trend raises questions about whether life insurers could end up being more involved in wellness and condition management programs than health insurers are.

6. Will the CVS-Aetna marriage work out?

CVS Health acquired Aetna with the idea of expanding CVS involvement in health care delivery. But Walgreens has raised questions about the future of retail clinics in drug stores by shutting down more than 100 of its in-store retail clinics.

The fate of the Walgreens retail clinics has led to followup questions about why CVS Aetna clinics would work better than Walgreens retail clinics.

7. Will discussions about adding long-term care benefits to the Medicare program heat up?

Some stand-alone long-term care insurance issuers are still out there trying to make the case that, after everything, stand-alone LTCI continues to be the most efficient private vehicle for protecting people against catastrophic long-term care risk.

But interest rates are still low. Securities analysts and rating agencies still take a dim view of the solvency of existing blocks of LTCI business.

Medicare program managers have been experimenting with adding tiny amounts of LTCI-like benefits to Medicare Advantage programs.

The major Medicare for All proposals include universal long-term care benefits provisions.

Could this be the year when long-term care finance policymakers recover from the failure of the ACA CLASS Act long-term care program and begin a serious effort to build long-term care benefits into Medicare?

Last Year’s Questions

1. How solvent are smaller players?

Value of question: Good.

Answer: Unknown.

2. Will anyone involved with Texas v. USA litigation figure out what’s in the Affordable Care Act?

Value of question: Good

Answer: The 5th U.S. Circuit Court of Appeals has just asked a trial court to look into that.

3, Will the stop-loss market take off?

Value of question: Medium

Answer: Unclear. To be determined.

4. How exactly will workers get paid?

Value of question: Poor.

Answer: Last year, ADP was suggesting that employers might shift to more flexible payroll schedules. At this point, this does not seem to be a hot topic.

5. What are plans doing about behavioral health benefits?

Value of question: Good.

Answer: Apparently, typical plans may be reducing the quality of behavioral health benefits.

6. Can short-term health insurers handle all of the new love?

Value of question: Good.

Answer: To be determined.

7. Will someone out there figure out how to get people to take care of themselves?

Value of question: Good.

Answer: It hasn’t happened yet. To be determined.

Read more: